How Venture Funds Source Deals

A Monthly Mini VC-MBA Series - Part 1 (September 2020)

(Intro: starting this month, I will start writing some evergreen topics of venture capital, on a monthly basis - in the hope of demystifying some of the VC terms but also to be helpful for entrepreneurs and aspiring VCs to gain a better understanding of how the venture capital mechanism works)

Deal flow is a venture fund’s lifeblood. Without it, a fund will make no investments, or worse, make bad investments. It’s really the foundation of venture capital.

There are five major ways to source deals [1] and I will break it down in the following paragraphs and explain the pros & cons and the unsaid dynamics/ psychology of each channel.

An aspiring VC/ angel investor can refer to some of the paths to generate her own deal flow. For an entrepreneur, hopefully, the list can point the direction to get her company in front of investors.

The common deal sources are: 1) Networks; 2) Demo Day / Accelerator; 3) University/ Corporate R&D; 4) Industry / Hobby Conferences; and 5) Proactive outreach / “cold calls”.

We will go through each of them one by one, except the last point number 5 as it represent an active sourcing / hunter’s approach that deserves a separate post.

1 - Networks

Networks have been a major funnel for VCs to get deal-flow. Ever heard of a VC saying that “The best way to get in touch with me is to get an introduction from someone I know.”? [2] I bet more than a few times. So why is that?

Talents tend to cluster. And capital follows.

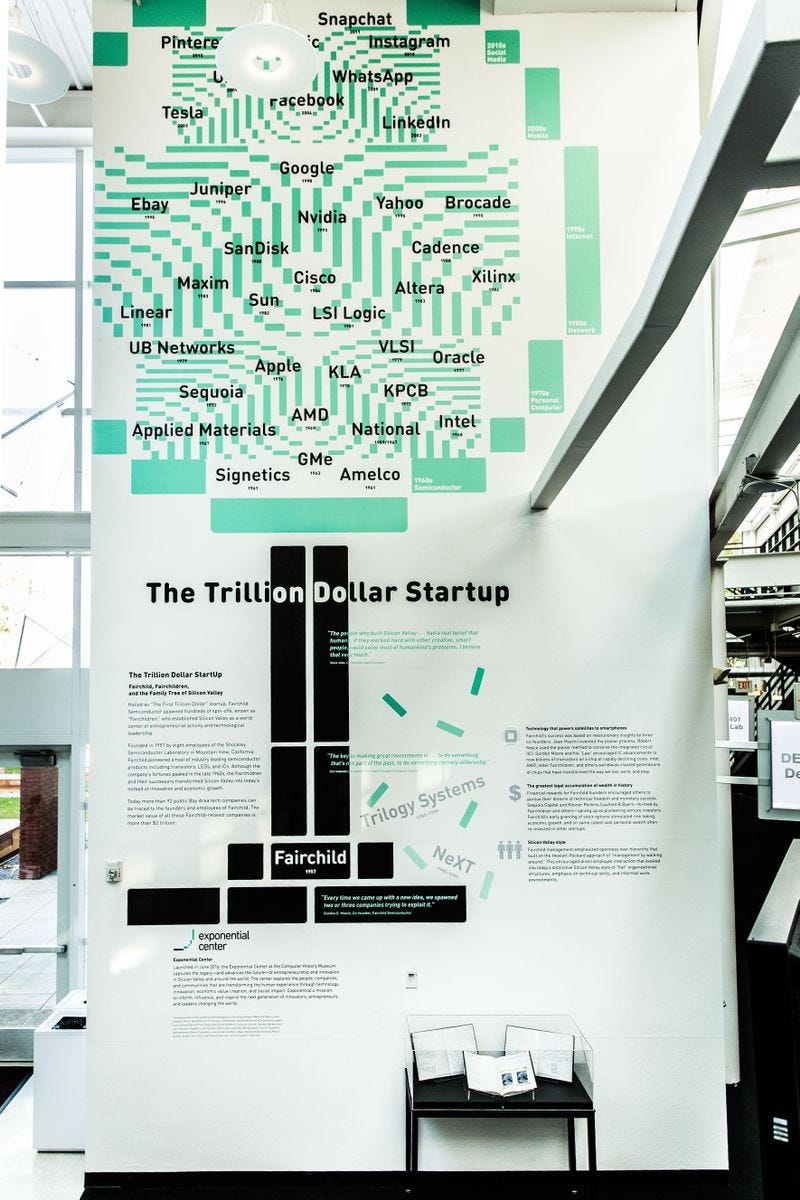

To understand this, you have to understand the root of the VC industry. Founded in 1957, Fairchild Semiconductor proved itself to be the mother of Silicon Valley - it not only gave births to other iconic companies (called “Fairchildren”) such as Intel and AMD, it also can be attributed to the founding of Sequoia Capital and KPCB, of which both founders have association/ ties with Fairchild. [3]

(Silicon Valley family tree in Computer Science Museum, Mt View, CA)

Later on, the tech infrastructure provided by the ones like Intel and the capital offered by the ones like Sequoia, fostered the rise of category-defining companies in the 90s and 2000s - Sun Microsystems, Cisco, Netscape, Google, Facebook, LinkedIn, etc. - that we know today.

It doesn’t end there. On the flip side of founders, the funders have deeply intertwined roots as well. Jerry Neuman, a professor at Columbia and also a friend, documented the genealogy of VC funds as well.

As you can see, both talents and capital are clustered by networks and relationships. And it’s not by intentional design. It was built into the DNA at its origin.

This way of deal sourcing has its advantages, in that it’s fairly efficient as your network would already give the company a first or second-degree screening before you are meeting the company. In addition, as a VC builds her brand profile, her deal quality from the network referral - in theory - would increase as well.

It’s worth noting that even within the network referral, intros from different parties do carry a different weight from a VC’s point of view. I will rank them from high score to low.

Founders /entrepreneurs network. Similar to “peer review” in academic settings, VCs love to get to know a new entrepreneur who is endorsed by her fellow peers. VCs believe that “talents tend to cluster”, that’s why a warm intro from a VC’s existing portfolio founder is likely the best setup for a new company intro.

School/ company Alumni network. Though not always true, a school/company not only pre-select a group of similar people, but it also provides an environment to shape a specific culture. That’s why you are seeing schools like Stanford, MIT, Berkeley, and Tsinghua tends to produce tech entrepreneurs sustainably. On the company side, the most well-known example is the “Paypal Mafia”, which include the founders of Linkedin, Yelp, Youtube, SpaceX and Tesla. VCs have been trying to identify the next tech mafia but so far, none is on par with the the Paypal one.

Peer VCs network. It really depends on how well the two VCs know and trust each other. VCs are a group of skeptics. The common psychology at play here are: “why am I getting the deal?” “If the deal is so good, why isn’t she investing/leading the deal?” However, if the VC who makes the introduction has a great reputation and thought leadership, the referral can be useful.

Service providers network - i.e. accountant, lawyers, advisors. This route is more neutral from a VC’s POV: since on one side, “any client who is paying me $500 per hour is great” and on the other side, the service vendors, although not professional investors, do put some thoughts and filter to the companies that they recommend. VCs often take them as additional deal flow - no more, no less.

However, there are obvious downsides to this overall “networks” approach as well:

a) you are only seeing what is being presented to you. It’s a passive approach.

b) it can easily lead to group thinking or worse, elitism. It’s comfortable to be surrounded by people who look, think, and act like yourself; but that’s not how progress is made.

In the US, Steve Jobs of Apple, Brian Chesky of Airbnb, and Jan Koum of Whatsapp are all outsiders, belong to no “mafia” and yet, they created some of the category-defining companies.

In China, which enjoyed the long fruitful growth over the past decades, the list can go even longer: from Jack Ma of Alibaba, Pony Ma of Tencent, Liu Qiangdong of JD.com, and Yiming Zhang of Bytedance.

It is the misfits who make 80% of the power-law returns.

c) Lastly, a VC who relies too much on her networks tends to suffer from the trap of herd mentality / social proof. And unfortunately, it’s a common psychology flaw among VCs. Founders often times can use this to exploit the investors by saying “So and so have invested and we are closing quickly…”

2 - Demo Day / Incubator / Accelerator

The Demo Day concept was taken into the mainstream by the famous YC. Started in the mid-2000s, YC incubated iconic companies include Airbnb, Cruise, Twitch, DoorDash, Instacart, PagerDuty, Dropbox, Gitlab, etc.

(Early days of YC - Dropbox presenting in 2007)

These are all great companies that pretty much defined the modern internet in the Cloud Age. Looking back, accelerators like YC started in a great timing as the infrastructure of the Cloud had collapsed the costs of starting a tech company and therefore enabled entrepreneurs everywhere and anywhere.

Comparing to VC’s traditional “I will take a meeting if you can get an intro” approach, YC took meetings based on startups’ minutes-long video interview.

A simple idea at the time, but powerful as it turns out.

YC’s “open-door” approach solved the bottle of the "networks” channel and therefore captured many "under the rock” diamond entrepreneurs that were, at the time, underserved by the big-name VC firms [4].

Having entrepreneurs as customers to serve, venture capital funds need innovation as well; and YC in 2005, probably unconsciously, did just that.

Fast forward to now, accelerators and Demo Days are in again. Over the past 10 years, it’s not uncommon to see investors cram themselves into a “small room” at the Computer Science Museum in Moutain View or Pier 48 in San Francisco, or more recently over a private Zoom link.

(The latest in-person YC Demo Day in 2019)

So if you are a founder who is coming from the outside, it might not be a bad bargain to join a reputable accelerator in exchange for giving up small equity.

A well-run Demo Day can create the perfect asymmetry between investors and founders [5], in that startups can quickly leverage the momentum to close funding quickly.

However, just like most things that operated in the startup/venture universe, not every accelerator/demo day is equal. They are very much like colleges - the best-branded institute, like YC, tends to absorb the majority of talents.

But could the accelerator network become so big or so exclusive that it becomes just one of the “networks” as we discussed prior? It would be interesting to see if and when the initial “open-door” advantage begins to wear off and has diminishing returns.

IMHO, the hit rate is the key.

Comparing to the small demo days (8 companies presenting to 15 investors) held by YC in 2005, we now have thousands of accelerators globally and each demo day has more than 100 startups presenting. And this scaling-up trend is not slowing down [6].

3 - University and Corporate R&D

This is a channel that’s less emphasized in the VC deal souring funnel. But it has its importance. In the US alone, R&D spending by universities and corporates amounts to $260B annually. Spinoff startups often carry the researchers’ DNA, which usually works well for deep-tech oriented companies. But to a VC, the holy grail is to see the perfect combination of tech superiority and acute business acumen - the later is harder to find in the R&D settings.

But once in a while, you might just wander into a university project called Stanford “Backrub” (assuming you can time travel to 1996), which was the origin of Google. Nowadays, it’s not uncommon to see VCs spending time in the labs or hold events with Post-Docs.

Going forward, with the proliferation of AI and deep tech, we expect to see more quality deal potential to be unleashed from university labs. I, for one, pay close attention to this.

On the corporate side, it’s a bit complicated. Corporates’ R&D initiatives are often times tangled with internal politics and their external spinoff efforts can find themselves a hard time recruiting the best talents. At the end of the day, corporates are not well designed to spot emerging market trends AND execute on it.

Despite that, VCs can often get interesting leads by paying attention to this direction.

For example, Apple was partially “allowed” to be created because HP turned down Steve Wozniak’s internal proposal for personal computers. In the technology dance, the missteps of the incumbents are blessings to the little guys. Another example is Xerox’s underappreciation of its own User Graphic Interview (GUI), which was later monetized by (again) Apple.

Nowadays, the corporates are getting smarter by setting up their own venture arms and even incubators to combat those bad knee reactions. Some are fairly successful such as Google, Qualcomm, and Microsoft - who typically have both proprietary tech and market-driven incubation processes in place. And VCs would love to be in the mix, leading or participating in the deals that are incubated by them. [7]

4 - Industry / Hobby Conferences

Companies and customers gather around industry/hobby conferences. And VCs follow. Some of the bigger, more well-known ones are CES (for consumer electronics), GDC (for gamers), RSA (cybersecurity), MWC (mobile), Techcrunch Disrupt (startups), Money20/20 (fintech), to name a few. They typically have a large Expo area where both customers and investors can walk the floor and see what the latest trends are all about.

These events are usually pre-booked on a VC’s calendar every year. And given the growing scale of these big conferences and all the social “mixers” that are held during the events, they often become more of a networking / catching-up setting for VCs rather than deep-dive learning opportunities on vertical topics [8].

Personally, just like the startups that we seek, I prefer being in the mix of emerging communities. Those are made out of a few passionate enthusiasts who are either the organizers or the thought leaders in the group. You can think Homebrew Computer Club where Steve Wozniak of Apple demoed its first prototype as one of the early hobby communties. By definition, these communities are not big but highly cohesive.

(In a 2014 Bitcoin conference, the gentleman on the upper left was live auctioning Bitcoin at $120 apiece… How outrageous! I’m sobbing as I dug out this photo from my old phone :(

Another example would be the Bitcoin / Crypto community in the early days of the 2010s. A few years after Satoshi Nakamoto published the Bitcoin whitepaper in 2008, small enthusiasts communities emerged - they consisted of hackers, scholars, and economists [9].

It was easy to dismiss these groups of people as hobbyists who were just “play around” with this “fictional money”. But fortunately for me, I was tasked to understand Bitcoin better for my job (basically, paid to learn!), so I immerse myself in all those crypto events and communities, which led me to meet with a lot of early crypto thought leaders including Vitalik of Ethereum who I got to host in my office when they visited the valley in 2013.

(A meetup event hosted by yours truly, with Ethereum co-founder and other investors)

So for a VC fund, good coverage of small emerging communities is arguably just as important as being present at big conferences. Both provide different angles of opportunities for VCs to learn and - if you are lucky - to make good investments too. [10]

Summary

So there you have it - the four major channels to a VC fund’s deal flow [11]. Together they represent how a VC fund sees the ever-evovling waves of tech innovations.

The beauty of VCs’ deal-sourcing game is that there is no golden rule to a VC playbook and each investor has different takes / preferences on the above channels.

One famous saying goes the future is already here, it’s just not evenly distributed yet. We all try to be on the early side of the curve, to see the future a bit closer and yet nobody truly knows the future.

But that pursuit of truth, my friend, is what keeps the game dynamic and fun.

If you like this post, you can subscribe here. New essays will be delivered straight to your inbox so that you never have to worry about missing one. Also appreciate your sharing and comments as well :)

[1] I don’t really like the term “deals” as it sounds so transactional but in the context of fund operation and investment, the term “deals” would do.

[2] As a founder-turned VC, I’ve always found it somewhat arrogant for VC to say that. But that’s beside the point.

[3] It’s interesting to look at the Genealogy of Silicon Valley https://www.chiphistory.org/698-silicon-valley-genealogy

[4] One might argue that should YC never exist, the efficient VC market will eventually find and fund the likes of Airbnb, Twitch, Cruise, etc. I’m not so sure, especially given YC’s scale and success hit rate of backing those companies.

[5] During YC’s last demo day in 2020, the investor/startup ratio is 10:1.

[6] Recognizing the importance of capturing unicorns at the infant stage, some venture funds are starting their own accelerators or operating on a hybrid model (e.g. Science that incubated Dollar Shave Club, Expa that was founded by Uber Co-founder, etc.). So how can investors get a clearer signal from an ever-increasing large sample base? Or will those signals only be discovered internally and therefore become more proprietary - which justifies VCs running accelerators themselves? Have VCs changed the battleground from “demo day” to “pre-demo day”?

[7] However, time will tell if this combination of incentive alignment works. The most high-profile case in this category is probably Waymo https://www.businessinsider.com/alphabet-waymo-raises-over-2-billion-first-outside-funding-round-2020-3

[8] Recognizing the inefficiency of various conferences, David Hornik, a GP at August Capital, decided to hold the “unconference" THE LOBBY on his own. The “invite-only” tickets are the hottest commodity in the Valley among founders and VCs.

[9] Back in 2012, no VCs were in the mix yet. Most VCs were busy making jokes about Bitcoin and how it’s tied to illegal drugs. I don’t blame them. I recall that my first ever purchase of Bitcoin was done through a MoneyGram location in a dark corner where I had to hand out cash without any idea where that money goes or if I will receive bitcoin back! Shady! But fortunately, I did get the Bitcoin back but that was the first and the last time I purchase Bitcoin that way.

[10] The advice I often give young VC analysts is to really blend themselves into various meetup/startup events and community (or better yet, host one!), because not only it will give analysts the first-hand knowledge on emerging tech trends, but also give them the robust deal sourcing advantage that their 60-year-old senior partner might not have.

[11] We will talk about the last deal sourcing approach- proactive outreach / cold calls / hustling - in a separate post.